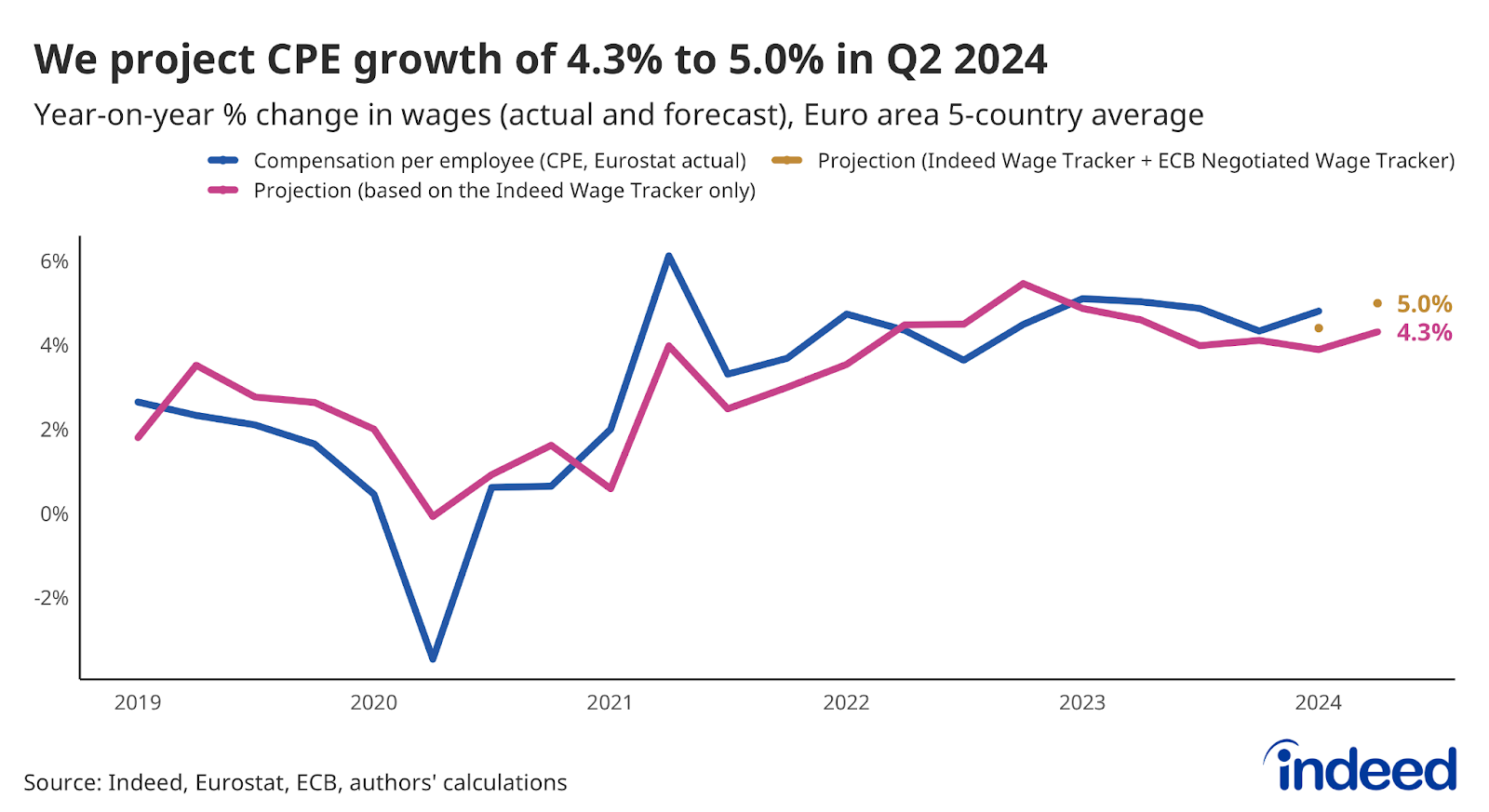

We expect annual growth in compensation per employee in the euro area to rise to 5.0% in the second quarter of 2024 before declining further.

Key Points:

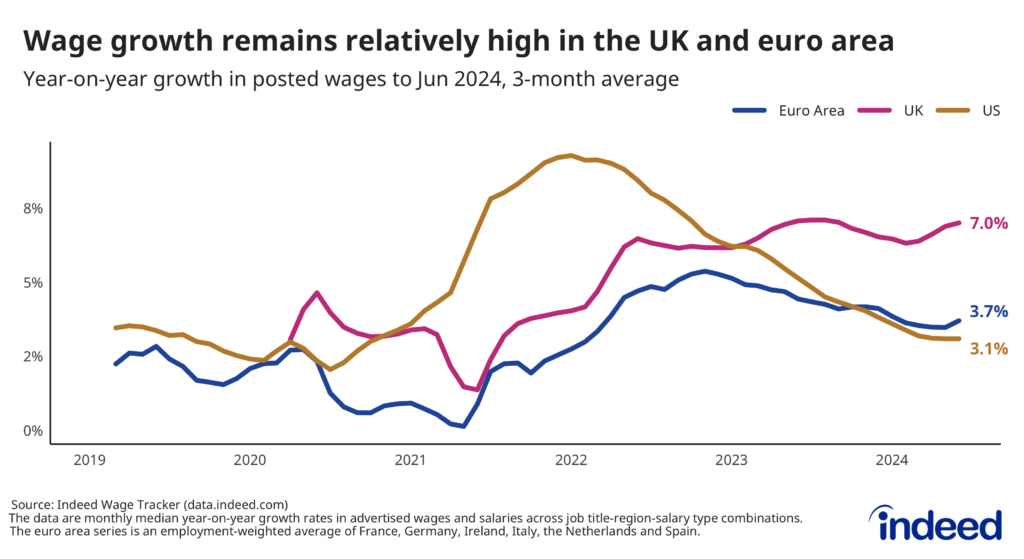

- Wages in job postings, as measured by the Indeed Wage Tracker, grew at an annual rate of 3.1% in the US, 7.0% in the UK and 3.7% in the euro area in June 2024.

- We estimate annual growth in total euro-area Compensation per Employee (which includes items not captured by advertised salaries, such as one-off payments to compensate current workers for past inflation) was 5.0% in the second quarter, up from 4.9% in the first quarter. While this is still notably lower than the post-pandemic peak of 5.5% reached in 2023, it is a sign that aggregate wage growth is likely to remain high in the euro area through 2024.

June data from the Indeed Wage Tracker suggests that annualized wage growth in the US, the UK and the euro area appears to have levelled off – but at different levels and with very different implications for their respective economies. In the US, posted wage growth appears to have stabilised at pre-pandemic levels – a welcome sign of labour market normalisation. But posted wage growth in the euro area and the UK has seemingly stabilised at rates that are higher than pre-pandemic norms. And our new forecast suggests that total euro-area compensation costs as measured by the European Central Bank remained elevated throughout the spring and early summer and are likely to stay high in the near term.

As policymakers worldwide attempt to bring down the rate of inflation – which spiked in the years immediately following the pandemic and has stayed uncomfortably high despite the efforts made to contain it – wage growth has emerged as one of the key inflation uncertainties. As global supply chains have normalised and the goods shortages that characterized the early years of the pandemic have faded, the attention of policymakers has turned to domestic drivers of price increases. Wages are an important driver of domestic inflation, both from a demand perspective (supporting consumption) and a supply perspective (raising firms’ costs). The latter is especially relevant in the services sector, where wages account for a greater share of input costs, and where inflation has generally been stickier in recent months.

Wage growth appears to be stabilising rather than continuing to fall

Annual euro-area wage growth stood at 3.7% in June, according to the Indeed Wage Tracker, down from a post-pandemic peak of 5.4%, up slightly from 3.5% in March, April and May, and still well above the pre-pandemic range of 2% to 2.5%. The general but hardly uniform downward trend in euro-area wages reflects the staggered nature of real-wage catch-up resulting from collective bargaining in Europe. This also partly explains why annual euro-area wage growth has been broadly flat since the start of 2024, moving in a tight range of 3.4% to 3.8%.

In the UK, annual wage growth in June ticked up to 7.0% from 6.9% in May, just below its recent 2023 peak of 7.1%. Strong UK wage growth is evident across all pay ranges for low, medium and high-paying jobs. While headline UK inflation is in line with the Bank of England’s target for the first time in three years, the elevated rate of wage growth remains concerning to some monetary policymakers who worry it indicates sustained domestic inflationary pressures.

Annual US wage growth in June was 3.1% for the third consecutive month, showing signs of stabilising at the pre-pandemic level. If this levelling off continues in the coming months, it will be a sign that the US labour market has successfully rebalanced.

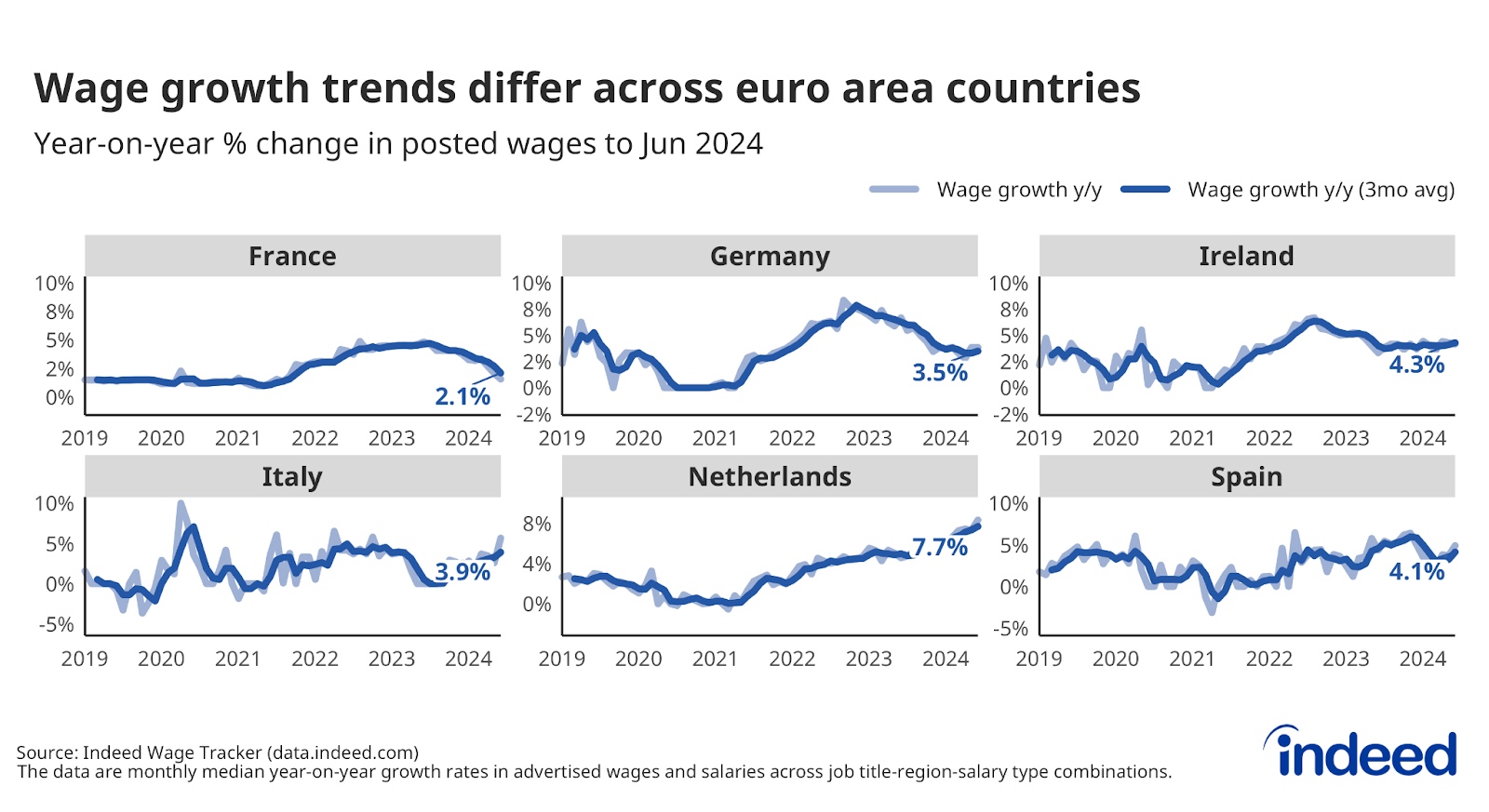

Our euro-area wage growth estimate is an employment-weighted average of six countries – Germany, France, Ireland, Italy, the Netherlands and Spain – that collectively account for approximately 80% of euro-area employment. Recent trends differ across these countries. Wage growth has been stable or falling in France, Germany and Ireland, and is already at or close to pre-pandemic levels in those countries. But in Italy, the Netherlands and Spain, wage growth has been picking up and remains high relative to national pre-pandemic averages.

Spotlight: Euro area wage growth in Q2 2024

The ECB projects wage growth as part of a broader measure known as Compensation per Employee (CPE), which is constructed from national accounts data and released at a long lag. For example, aggregated euro area CPE for the first quarter of 2024 was published as part of the national accounts release on 7 June, and official data for the second quarter will not be published until 6 September. This wide gap between the end of the quarter and data publication is a problem for policymakers, especially in times of elevated uncertainty.

But monthly data from the Indeed Wage Tracker is available shortly after the end of each month, and we have used it to construct more timely, near-term projections for year-on-year growth in CPE in the second quarter of 2024. Our projection for Q2 2024 is 5.0% when information from both our wage tracker and negotiated wage data is included in the model and 4.3% when we based it on our wage tracker only.

Our headline forecast of 5.0% CPE growth includes negotiated wage data because incorporating this information creates a closer match with CPE in the historical data sample to the end of the first quarter of 2024. This makes intuitive sense if wage agreements include things like one-off cost-of-living payments or back-dated real wage catch-up that may not be captured in advertised wages and salaries but do affect the total pay of current workers (i.e., the basis of the CPE estimate). In general, we find that the negotiated wage data improves the projection the most in Germany – where one-off payments have tended to be larger in recent months – but plays less of a role in the other countries. A projection based only on negotiated wages performs very poorly historically, so the Indeed Wage Tracker is a key component of our forecast. See the methodology section below for more details.

Our headline forecast of 5.0% CPE growth is only slightly below the ECB’s most recent projection of 5.1% for the second quarter. An important caveat is that the ECB publishes projections for the euro area as a whole, whereas our projection is for the five euro area countries for which we have Indeed Wage Tracker data at the occupational level (Ireland is excluded for data availability reasons). That said, these five countries are an important driver of total euro-area figures since they represent almost 80% of euro-area employment.

The ECB’s June projections expect wage growth (as measured by compensation per employee) to remain elevated throughout 2024, averaging 4.8% for the year. Our Q2 projections for CPE growth – based on new Indeed Wage Tracker data to June and the ECB’s negotiated wage tracker – support this narrative. For the second half of the year, the ECB expects wage growth to slow to 4.7% in Q3 and 4.5% in Q4, partly on the basis of forward-looking information in its negotiated wage tracker. This, combined with the continuing decline in job posting volumes, suggests demand pressures in the European labour market are gradually easing. And as the real wage gap closes, one-off payments will likely play less of a role in pay agreements. This will likely close the gap between the Indeed Wage Tracker and negotiated wages. As such, we expect CPE growth to start moving closer to our projection without negotiated wages, i.e., the low 4% range.

Conclusion

Policymakers assessing the path for inflation are paying close attention to wage developments as a potential source of persistent inflation pressure. The Indeed Wage Tracker shows a gradual easing of wage growth throughout 2023 in the US and euro area, followed by a rebound in the UK and somewhat of a plateauing in the euro area and US in the second quarter of 2024.

Our projections, based on advertised wages and salaries captured by our tracker and additional information from collective bargaining agreements, suggest year-on-year growth in compensation per employee in the five large euro-area countries tracked will be 5.0% in the second quarter – below its post-pandemic peak of 5.1% in 2023, but still high compared with the 2019 average of 2.2%. Our current forecast thus supports the ECB’s expectations that CPE growth for the euro area as a whole will average a fairly elevated 4.8% during 2024.

Methodology

To construct the forecast of euro-area CPE growth, we use all available Indeed Wage Tracker data at the country and occupational level. We first identify an optimal weighted combination of occupational-level wage growth that provides the closest match to historical CPE growth trends through Q1 2024. We then use these optimal weights to project CPE growth for the second quarter of 2024, taking advantage of the already published Indeed Wage Tracker data to the end of June. Additionally, we incorporate information from the ECB’s Negotiated Wage Tracker to improve the accuracy of the projections.

In the historical data, the Indeed Wage Tracker does a very good job of tracking CPE dynamics. Because of pandemic-related volatility in the compensation of all workers, in part driven by government payment schemes, the second quarters of 2020 and 2021 are an exception.

To calculate the average rate of wage growth in the Indeed Wage Tracker, we follow an approach similar to the Atlanta Fed US Wage Growth Tracker, but we track jobs, not individuals. We begin by calculating the median posted wage for each country, month, job title, region and salary type (hourly, monthly or annual). Within each country, we then calculate year-on-year wage growth for each job title-region-salary type combination, generating a monthly distribution. Our monthly measure of wage growth for the country is the median of that distribution. Alternative methodologies, such as the regression-based approaches in Marinescu & Wolthoff (2020) and Haefke et al. (2013) produce similar trends.

The euro-area figures are an employment-weighted average of growth rates in France, Germany, Ireland, Italy, the Netherlands, and Spain. The weights for the most recent months are revised periodically as new employment figures are published by Eurostat.

All wage growth figures mentioned in this post are three-month averages unless stated otherwise.

More information about the data and methodology is available in two research papers. The first, by Pawel Adrjan and Reamonn Lydon, What Do Wages in Online Job Postings Tell Us about Wage Growth?, describes the construction of the Indeed Wage Tracker and is forthcoming in Research in Labor Economics in 2024. The second, Quarter-Casting Euro Area Wage Growth, by Pawel Adrjan, Reamonn Lydon and Vahagn Galstyan, shows how the Indeed Wage Tracker can be used to compute near-term projections for growth in compensation per employee. Wage growth series are available for download in the Hiring Lab Data Portal.

Wage Growth Has Slowed but Remains High in Much of Europe – And Looks Poised To Stay That Way in the Near Term #Wage #Growth #Slowed #Remains #High #Europe #Poised #Stay #Term

Source Link: https://www.hiringlab.org/uk/blog/2024/07/10/wage-growth-in-europe-remains-high/

WP8, Europe, growth, High, poised, Remains, Slowed, stay, Term, Wage – Wage Growth Has Slowed but Remains High in Much of Europe – And Looks Poised To Stay That Way in the Near Term – #WP8

We expect annual growth in compensation per employee in the euro area to rise to 5.0% in the second quarter of 2024 before declining further. Key Points: Wages in job postings, as measured by the Indeed Wage Tracker, grew at an annual rate of 3.1% in the US, 7.0% in the UK and 3.7% in …