imaginima

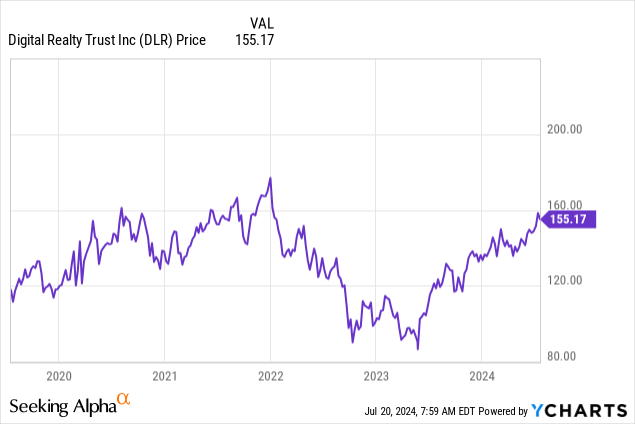

Since I last covered Digital Realty Trust (NYSE:DLR) in February 2021 in a piece entitled “Expanding To Greener Pastures”, it had gained 25% by December as a beneficiary of the digital transformation trend, before plunging as the Fed tightened rates aggressively. Since then, the stock has gone up and trading at around $155.

This thesis elaborates on its AI opportunities, namely for hosting accelerated computing to support supersmart applications. Also, contrary to my earlier hold position because of the debt, this time around, I am bullish because of the capital-light approach.

Also, with the company reporting second-quarter 2024 (Q2) earnings next week, I make the case for both revenue and FFO beat, but first, explain how DLR’s role should evolve from a cloud data center provider to more of an AI factory as Nvidia (NVDA) sells billions of dollars worth of advanced chips.

The Emergence of AI Factories To Support Super Smart Apps

Since the advent of OpenAI ChatGPT in November 2022, Generative AI has been making its way into our daily lives, initially for searching purposes. Still, this innovation should form part of almost every app we use as it gets embedded in video editors on our phones with Apple (AAPL) Intelligence, productivity software with Microsoft’s (MSFT) Copilot on our laptops, or intelligent assistant for social media with Meta Labs (META).

For this to happen, data centers will have to support tremendous numbers of accelerator GPUs (graphics processing units) whether those from Nvidia or Advanced Micro Devices (AMD) which tend to consume up to twice the amount of conventional CPUs normally supplied by Intel (INTC). This means energy has now become an important element, starting with the AI training phase where algorithms are trained with data right to the inference part where software developers develop applications.

This underscores the need for the AI factory, where large capacity blocks of data center space are provided to customers by DLR for deploying the compute together with contiguous data sets while enabling them to be adjacent to their users and cloud providers.

Corporate presentation (static.seekingalpha.com)

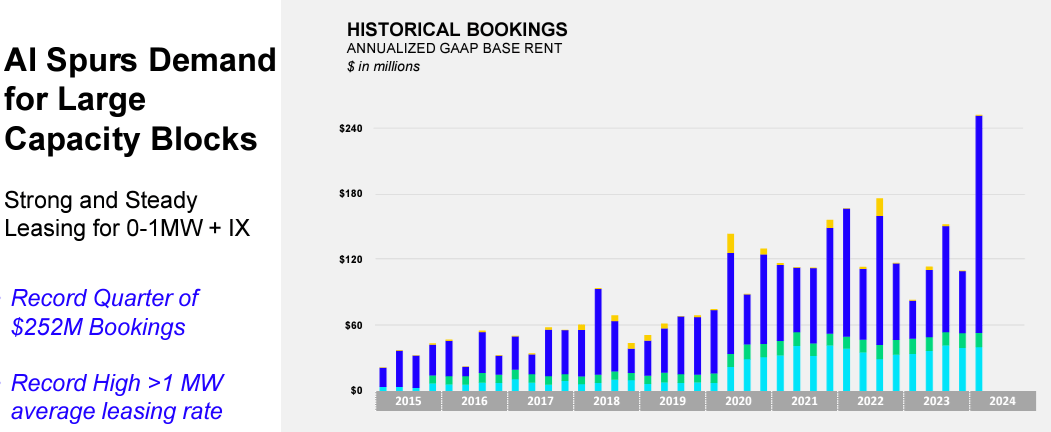

To obtain an idea of the momentum, according to Gartner, Gen AI-fueled spending on data centers should accelerate by 10% this year compared to 4% in 2023. Moreover, most of this is for the planning phase of AI, implying more will be spent on the actual deployments next year. Such interest in innovation has resulted in the 50% increase in DLR’s bookings for the first quarter of 2024 (Q1) being AI-related.

Factoring In The Competition

However, in contrast to cloud computing, the requirements of AI especially from a deployment perspective are different from the traditional hyperscale deployment which has historically required data centers to be closely located together to reduce latency, or slowness between applications communicating with one another. This favored the emergence of big metro areas like North Virginia or Dallas, major markets where DLR is present.

Corporate presentation (static.seekingalpha.com)

In this connection, power utilities have enforced restrictions for data center development in certain metro areas, implying that power costs will become more expensive. Additionally, retrofitting, or refurbishing old data centers with new power and cooling equipment can be costlier than erecting new facilities.

In this regard, by taking advantage of AI training being more tolerant to latency and is, therefore, less location sensitive, Applied Digital (APLD) which was previously a Bitcoin mining hosting provider has built an AI data center in North Dakota where it has easy access to renewable sources of energy. This means that in addition to giant Equinix (EQIX), DLR faces emerging players competing for a piece of the AI pie. Furthermore, supply chains for everything from power generators, and transformers to substations have become stretched because of high data center demand.

Therefore, the transition from hosting cloud computing workloads to AI implies challenges and additional investments, and given DLR’s debt load, some may doubt its capacity to deliver rapidly.

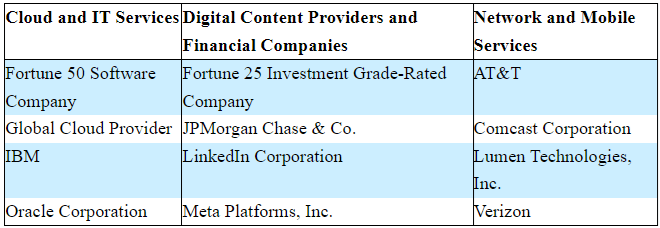

However, with more than 20 years of experience in the game and already boasting a customer base consisting of global cloud providers (or hyperscalers) and other big names as shown below, the REIT has an elaborate supply chain. Also, despite the energy bottleneck in North Virginia, its long-term partnership with the utility provider has allowed it to support customers’ hosting needs and in case of urgent need, it is also looking at the natural gas turbine option.

SEC Filing 10-K (seekingalpha.com)

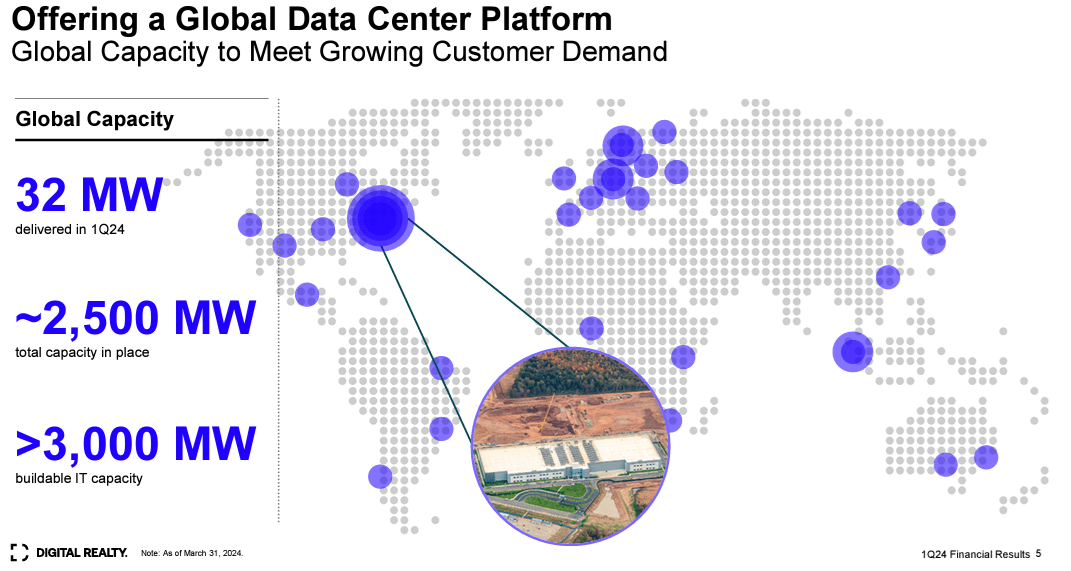

Moreover, instead of purchasing power at higher prices, it can capitalize on investments already made years ago, both for equipment and land that lies adjacent to existing facilities. Additionally, it disposes of 3 GW (gigawatts) of buildable IT capacity in 50 metro areas, implying agility to build AI data centers.

Deserves Better Based on FFO and Earnings Beat For Q2

Furthermore, with higher AI-related demand, hosting prices have increased significantly, from $80-90 per KW/month to $150-$160 KW/month or by 82%. This should translate into more profits, contributing to better net income and FFO (funds from operations).

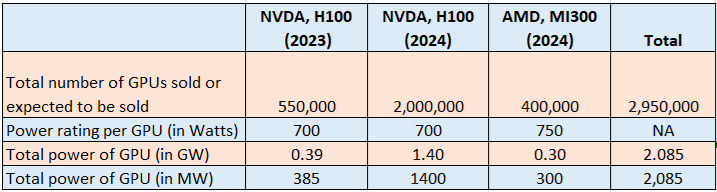

Now, to figure out AI hosting opportunities, I consider that Nvidia may have sold 550,000 GPUs in 2023 and 2,000,000 more is expected for 2024. Adding to the 400,000 expected to be sold by AMD and multiplying by their respective power ratings, or 750W for AMD’s MI300 and 700W for Nvidia’s H100, the total comes to 2.085 GW or 2,085 MW as shown below.

Table built using data from (seekingalpha.com)

Assuming that as the world’s largest data center, DLR gets to host 60% of this capacity or 1.251 GW by end-2025 (since there is a time lag between when chips are purchased, and they become operational), this will add 50% to its current capacity of 2.5GW, or 2,500 MW as shown in the Global capacity diagram above. On top, AI-related hosting generates 82% more revenue than conventional IT as mentioned earlier, increasing the net income and FFO.

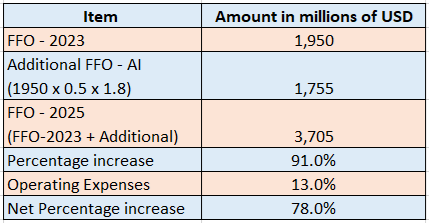

Now, $1,950 million in FFO was generated in 2023, and after adding the AI-related component as shown in the table below, the FFO for 2025 comes to $3,705 million, or a 90% increase. Subtracting for a 13% increase in operating expenses or the same percentage in 2023, I obtained a net increase of 78%, which means that the AI infrastructure play deserves better.

Table built using data from (seekingalpha.com)

Now, its forward price-to-FFO is already overpriced relative to the real estate sector by 68%, but it could still appreciate by 10% or (78%-68%). Therefore, incrementing the current share price of $155.17 by 10%, I obtain a target of $170.7.

This bullish position can be justified by upside catalysts, namely potentially beating expectations for the forthcoming second quarter (Q2) financial results next week. In this case, the consensus analyst estimate for FFO is $1.64 which would represent a 2.36% YoY decline while the revenue projection of 1.38 billion is for a modest 1.04% increase. However, as a beneficiary of AI and with better pricing and “continued strength in fundamental conditions” across its data center portfolio, expectations could be exceeded, thereby producing a beat.

There are Risks but the Capital-Light Approach Helps

Still, success will ultimately depend on executing both the artificial intelligence and cloud computing fronts, and this is the reason why I envisaged a long-term perspective. At the same time, due to the multi-billion-dollar investments required, it is important to assess capital allocation priorities, especially at a time when interest rates remain above 5% for a company holding $19.4 billion of debt versus only $1.19 billion of cash.

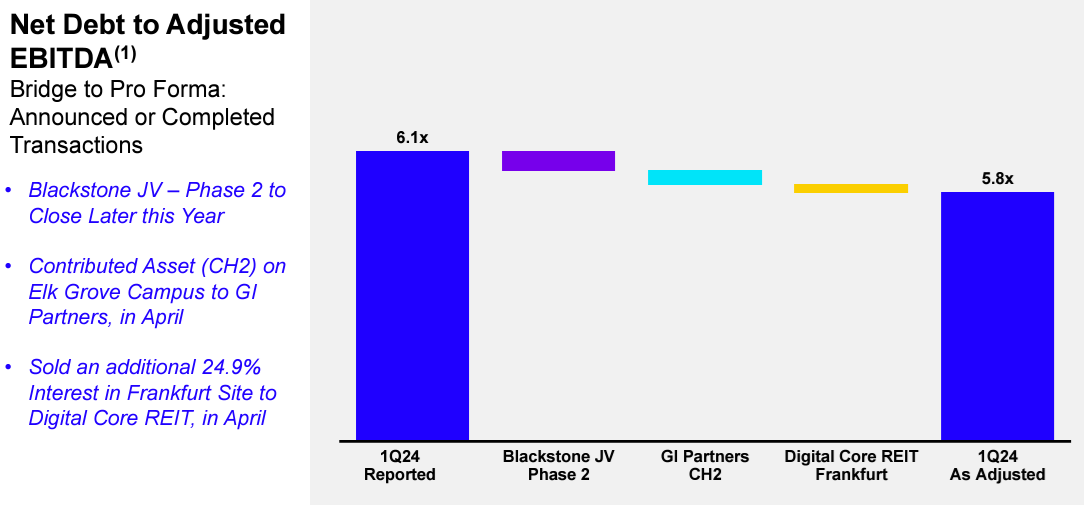

In this connection, instead of borrowing at higher rates, DLR has evolved its funding strategy to include joint ventures. Two of them were with Realty Income (NYSE:O) to build two data centers in northern Virginia, and Mitsubishi again for two data centers already under construction in the Dallas Metro Area. In each case, the partner is investing $200 million and the facilities will be ready this year. Looking at the longer term, a $7 billion agreement for 500MW (0.5 GW) of total IT load across 10 data centers was signed with Blackstone (BX) the world’s largest alternative asset manager, ensuring that the company can deliver IT capacity into 2025 and beyond.

Thus, inclusive of JVs and asset sales, $1 billion was raised, and this capital-light approach has resulted in leverage lowered from 6.2x to around 5.8x, ensuring that there is enough cash to invest without incurring debt.

Corporate presentation (static.seekingalpha.com)

Now one can argue that the JV approach entails returns having to be shared with partners, but, the financial burden and risk are shared. Also, thinking laterally, DLR will not only ensure day-to-day operations for which it will receive fees but also develop the assets adjacent to its other facilities like the 3 GW of capacity I talked about earlier, thereby creating cost synergies as it scales.

Coming back to the power estimates based on advanced chips making their way into data centers, 60% of the total being hosted by DLR may seem on the high side given the competition. However, these estimates are somewhat limited as they include only two GPU models and exclude both GPU estimates for 2025 and Intel’s Gaudi processors, but they help to have tangible figures as to the AI opportunities.

Along the same lines, DLR’s most important advantage is its experience and having rapidly adapted its data centers to support AI factories, which puts it in a suitable position to benefit from the four largest U.S. hyperscalers having expanded their Capex for 2024 by roughly 45% year-on-year to nearly $50 billion, or about nine times its revenue for 2023.

Ending on a cautionary note, with the demand being here, it is important to check whether the capital-light approach which has reduced leverage slightly stays on track during Q2’s earnings call around July 25. Also, it is important to obtain a management update on supply chain-related risks in case of higher import tariffs imposed on Chinese goods after the November elections and whether this will impact execution.

Digital Realty Trust: AI Factory Opportunities (Rating Upgrade And Q2 Preview) (NYSE:DLR) #Digital #Realty #Trust #Factory #Opportunities #Rating #Upgrade #Preview #NYSEDLR

Source Link: https://seekingalpha.com/article/4705336-digital-realty-trust-ai-factory-opportunities-rating-upgrade-and-q2-preview

Digital Realty Trust: AI Factory Opportunities (Rating Upgrade And Q2 Preview) (NYSE:DLR) – #WP10 – BLOGGER

imaginima Since I last covered Digital Realty Trust (NYSE:DLR) in February 2021 in a piece entitled “Expanding To Greener Pastures”, it had gained 25% by December as a beneficiary of the digital transformation trend, before plunging as the Fed tightened rates aggressively. Since then, the stock has gone up and trading at around $155. Data …

imaginima Since I last covered Digital Realty Trust (NYSE:DLR) in February 2021 in a piece entitl…